This article was written by four consultants for AlixPartners: Matt Hamory, partner and managing director and co-lead of its global grocery practice; Steve Scales, partner and managing director in manufacturing and operations; Yevgeniy Rikhterman, senior vice president in retail; and Pat Carroll, an independent contractor in manufacturing and operations and CEO of The CF Team.

New packaging fees — stemming from legislation approved by lawmakers in seven states and introduced in several others — are meaningfully decreasing the profitability of private brands and prepared foods, and grocers won’t be able to offset this new layer of costs unless they make changes that go far beyond packaging.

Extended producer responsibility laws — the origin of these new fees — shift to grocers the cost of waste management for packaging of any items sold under their own brands. The purpose of the legislation is to discourage the use of cheap, disposable packaging.

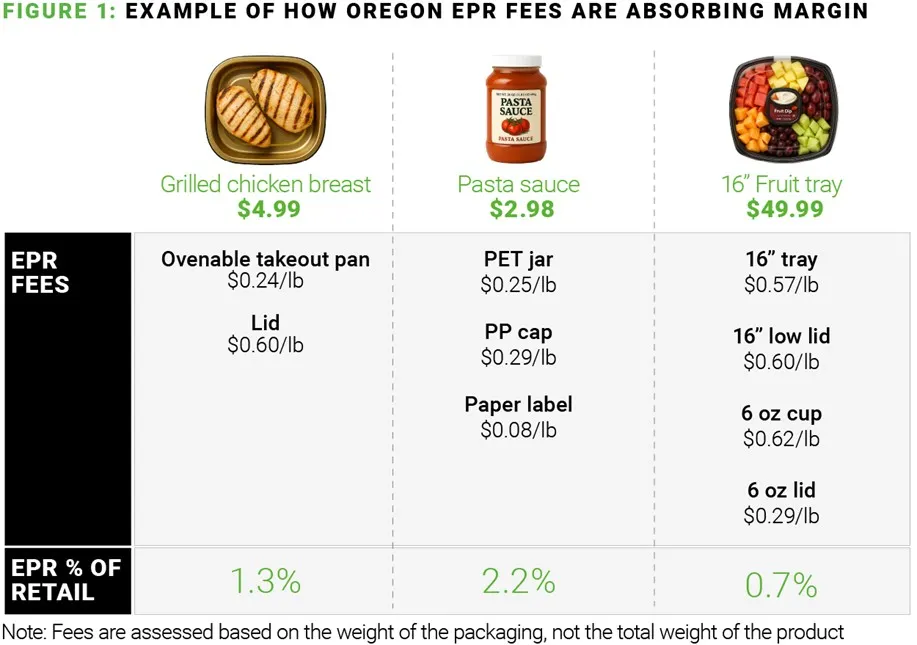

Our estimate, based on client experience, is that these fees will consume 1% to 2% of net sales — from 0.5% in meat to 6% in center store — when the amounts grocers will pay for their products and CPGs will pay for theirs are taken into account.

The added expense and compliance complexity posed by these fees would be enough of a challenge, but there’s a wrinkle: It should be assumed that the industry’s largest players have a multi-year head start on both the structural and strategic moves needed to navigate these changes.

The Circular Action Alliance, which was founded in 2022 to collect and administer the fees on behalf of the states, counts Walmart, Amazon, Target and the major CPGs among its charter members.

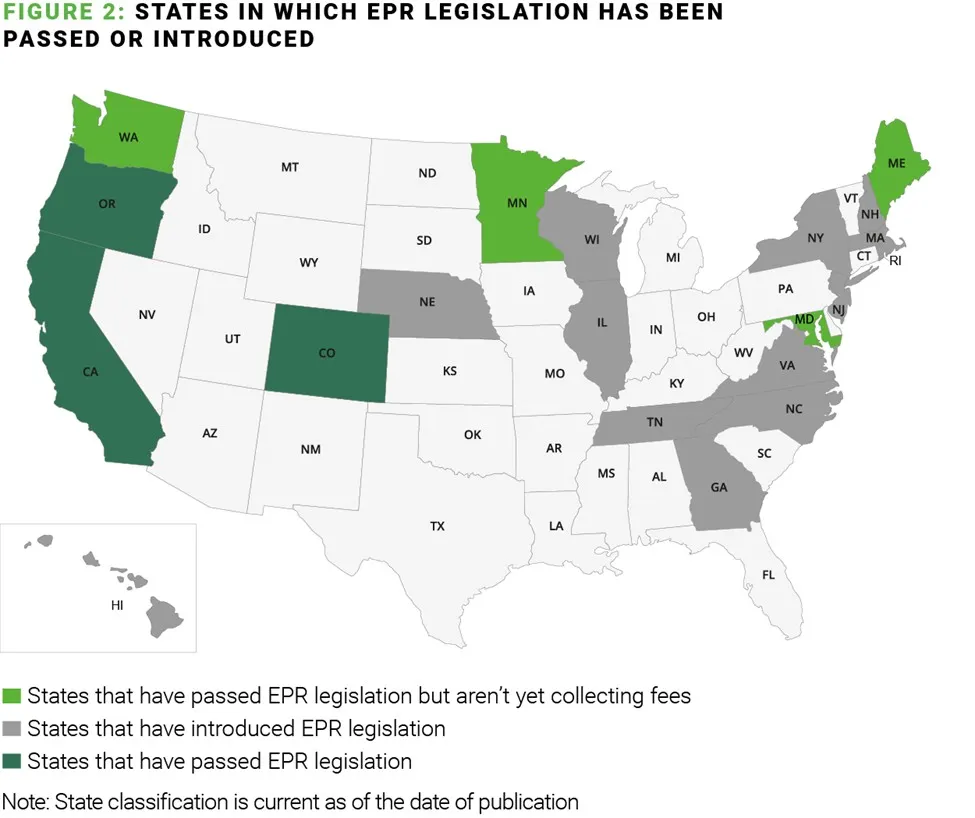

The states that have already passed EPR laws account for 21% of the U.S. grocery market. Include the states that have introduced legislation, and the number jumps to 48%.

Grocers operating in these states should be focusing first on compliance readiness and incremental assortment adjustments. Over the longer term, they will need to reevaluate pricing, manufacturing and assortment. Grocers will also need to decide what changes are needed now that baseline expenses are higher for two of the higher-growth components of the business.

First steps: Assessing exposure and achieving compliance

Data

Grocers will need to begin with an extensive data collection effort. Many items have multiple components subject to fees: A jar of peanut butter, for example, has a lid, seal, jar and label, and it would be highly unusual for category managers to already have a bill of materials that includes all packaging specifications in the format required by the administering body. All of that information has to be gathered, organized and evaluated.

Forecasting

Once grocers understand the fees that will be incurred by each item sold, they can forecast their total fees for a full calendar year. Estimating annual liability is essential because fees are only paid once a year — and that happens 13 to 24 months after expenses are incurred. For example, in Colorado and Oregon, reporting for 2025 is due May 2026, and grocers won’t receive invoices until January 2027.

Compliance

The compliance burden of these fees will be an ongoing additional cost, whether grocers develop an in-house capability to manage it or outsource to an expert third party. Missing reporting deadlines or payments will trigger considerable penalties, ranging from daily fines to, in some states, market prohibition.

Next steps: Considering long-term impacts and how to mitigate them

Pricing

Grocers will have to decide whether to pass these additional costs through to customers. They’ll also need to decide whether to allow their national brand suppliers to do the same. Doing both would raise the entire price architecture at a time when consumers are highly sensitive to value. Absorbing the higher costs, on the other hand, could mean a permanent reduction in margins.

Distributors face a particularly perilous road to navigate when it comes to these fees. With margins already low, further compression likely won’t be tenable, but neither will a straightforward passing along of higher costs. Identifying and implementing creative solutions in this area should be a high priority for this segment of the market.

Manufacturing

Grocers won’t be able to design away these fees completely, and they’re expected to increase every year. However, grocers can make changes to minimize costs throughout the value chain. In addition to lowering fee exposure by changing packaging material or reducing the amount of packaging — both of which are often much easier said than done — grocers should also reexamine total product cost.

Are there ways they can adjust recipes to lower cost without sacrificing quality? Can certain items be ordered more economically in different quantities? Can the manufacturer produce in larger runs that bring down the labor cost? Adjustments that stem from these kinds of questions can help offset the margin impact of the packaging fees.

Grocers with strong supplier partnerships will have an advantage in this effort. Those who rely primarily on third-party distributors can’t expect the same level of exploration and collaboration on changes across formulation, manufacturing, and logistics.

Assortment

Private brand items will need to earn their spots on shelves more than ever before. Grocers should consider rationalizing products that incur substantial packaging fees to the point where they break even or are only minimally profitable but don’t drive perception, differentiation or traffic.

For example, a grocer might keep a premium private brand of pasta sauces that is correlated with larger baskets and drop a similar mid-tier option that mimics the national brand, but delivers middling performance and is now less profitable.

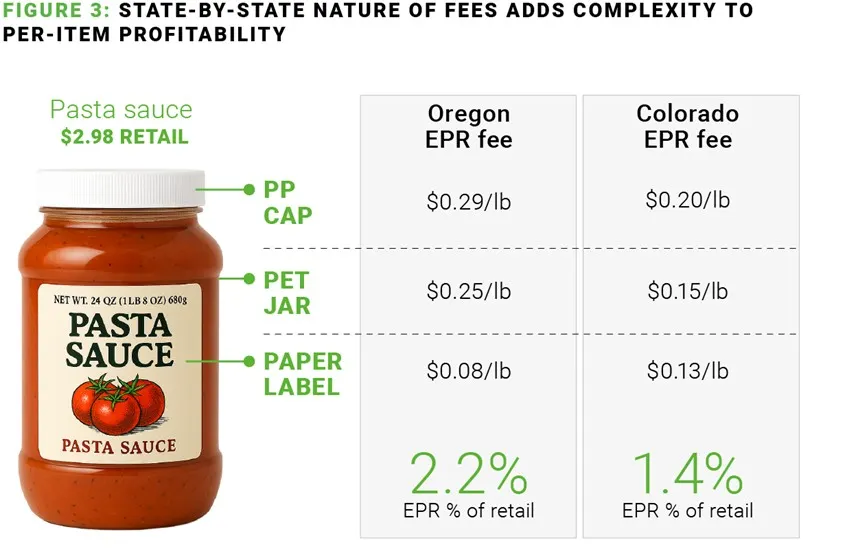

In addition, grocers that operate in multiple states will have to decide whether to switch packaging, formulation, manufacturing and logistics for all production based on the fees in certain states. They could also add complexity by producing items one way for some states and another way for others — or conclude that there are certain products they just won’t offer in states with EPR laws.

The road ahead

Because every state has different rules, assortments are constantly evolving and private brand and prepared foods are central to the growth strategy of many grocers, EPR readiness is quickly becoming a critical competency. These laws will disrupt many grocers, but the magnitude of the disruption is up to them. The faster grocers can define their liability and identify ways to reduce and offset it, the less disruptive EPR will be.